Do you really need that individual stock?

Individual stocks end up in portfolios for various reasons—possibly some speculation along the way, maybe inherited from a family member and kept for sentimental reasons, purchased many years ago and now with a cost basis so low that selling the stock would incur high taxes, or through acquisition of company stock options.

We don’t recommend buying individual stocks due to company-specific risk, and if you decide to buy a stock, you would not want to risk more than you can afford to lose. If you buy $10K worth of stock, you are unlikely to lose your lifestyle if the $10K goes to zero; at the same time, that $10K going up to $50K would be great, but it isn’t going to change your lifestyle either. If you decide to take a chance, you should ask yourself the following questions:

- Do you want the added stress and effort of watching and picking individual stocks?

- Do you think it is worth it to take on additional risk?

- Is buying and watching a stock something you enjoy doing regardless of the outcome?

We have all seen company-specific risks in the news on many occasions such as Twitter, Facebook/Meta, or Boeing and the 737 MAX disaster. It only takes one problem to tank a stock when everyone panics. We have also seen the negative effects of news in the past with Target and its 2013 credit card data breach (profit fell nearly 50% in its fourth fiscal quarter and the stock fell 9%) as well as with all the financial stocks that took a huge hit in 2008, such as Lehman Brothers, which ended up filing for bankruptcy. An interesting statistic—25% of stocks lost at least 75% in 2008 but only four of 6,600 mutual funds lost more than 75%. Even when it comes to IPOs, there is no guarantee that the price of the stock accurately reflects its true value.

One of the main academic theories we believe in is diversification, because it protects you from company-specific or business risk. While we know that the world markets trend up over time, the same cannot be said about a specific stock. None of the companies on the original Dow Jones Index are still a part of the Dow, and most have ceased to exist. The world is full of great companies that have had poor performance due to issues both in and out of their control. You should know the company’s revenues, expenses, P/E ratio, competitors, and a lot of other valuable ratios in order to decide if the stock is worth buying at the current price. Just because it’s a good company or a good idea does not mean it is a good stock!

Trying to pick stocks leads to an extremely high probability that you will underperform the market over the next 10 years. Over 90% of active stock pickers (these are highly trained specialists backed up by large research departments who get paid a lot of money and spend all their life trying to beat their index—yes, this is their day job) have failed to beat their respective benchmark over the past 10 years.

S&P Dow Jones Indices found that 89.4% of U.S. mid-cap stock funds, 85.5% of small-cap funds, and 66% of large-cap actively managed funds trailed their benchmarks in 2016. That came in a year in which stock markets performed well. If a fund manager can’t beat the benchmark and that is what they do all day, the odds are against you.

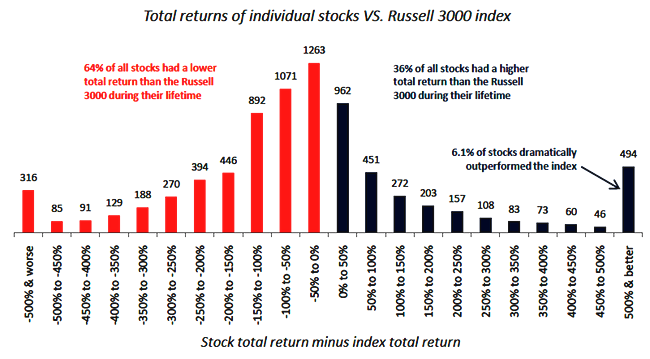

The following chart shows the lifetime total return for individual stocks relative to the corresponding return for the Russell 3000 Index. (The Russell 3000 Index is a market-capitalization-weighted equity index that provides exposure to the entire U.S. stock market.)

Source: The Capitalism Distribution – The Realities of Individual Common Stock Returns

by Eric Crittenden and Cole Wilcox, BlackStar Funds

The average retail investor who may spend a few hours a month researching stocks has no chance. They underperform the market and their own investments. You may get lucky, but the likelihood of underperforming index funds is quite high.

Categories

Recent Insights

-

Is FIRE Still Realistic?

The modern FIRE movement may be less about quitting work and retiring, and more about buying back your time.

-

Evensky & Katz / Foldes Wealth Management: Interview With Principal & Chief Revenue Officer David Evensky About The Advisory Firm

Evensky & Katz / Foldes Wealth Management is a registered investment advisory firm that provides comprehensive wealth management, financial planning, and investment advisory services to individuals, families, and institutions. Pulse 2.0 interviewed Evensky & Katz / Foldes Wealth Management Principal and Chief Revenue Officer David Evensky to gain a deeper understanding of the company.

-

Budgeting and Financial Organization: Lessons from Life, Love, and Messy Homes

Recently, my wife sent me an opinion article from The New York Times titled “My Home is Messy, and I Don’t Feel Bad About It” by KC Davis. The author highlights many reasons why being messy can be a positive trait—from fostering creativity to accepting that the same DNA that “makes us shine can’t be…

-

Talk Your Chart | 2026 Predictions: A Year in Review and a Look at the Year Ahead | Ep. 75

Episode 75 of Talk Your Chart kicks off the new year with Marcos and Brett revisiting their 2025 predictions to see what held up, what missed, and why. From stocks and bonds to GDP growth and Bitcoin, they break down the charts that mattered most and share their outlook for the year ahead. Charts available…

-

Private Family Foundations: A Legacy of Giving and a Classroom for the Next Generation

For families who want to make a lasting impact, a Private Family Foundation (PFF) can be both a philanthropic vehicle and a platform for teaching values across generations. At its core, a private foundation is a tax-exempt nonprofit organization that you create and control—one that supports the causes you care deeply about, both during your…