Financial Planning to the Rescue During Times of Uncertainty

Categories

Recent Insights

-

Before the Ballots: The Strategic Advantage of a SLAT During an Election Year

With less than 70 days until election day, the future of both the White House and the Senate hangs in the balance. Regardless of who wins, the ongoing challenges of rising federal deficits, unprecedented spending, and lower tax revenues could pave the way for higher taxes in the future. The estate tax exemption, which primarily…

-

Talk Your Chart | Fed Rate Cuts, Weak Recession Signals, and a Bull Market in Slow Motion| Episode 61

In Episode 61 of Talk Your Chart, Brett and Marcos explore the latest on the Dogs of the Dow, Utilities’ surprising rise, and Constellation Energy’s nuclear power dominance. Dive into the current bull market, Fed rate cuts, inflation signals, and why recession indicators remain weak.

-

Talk Your Chart | Monopolies, Markets, and Missteps: What’s Really Driving Prices? | Episode 60

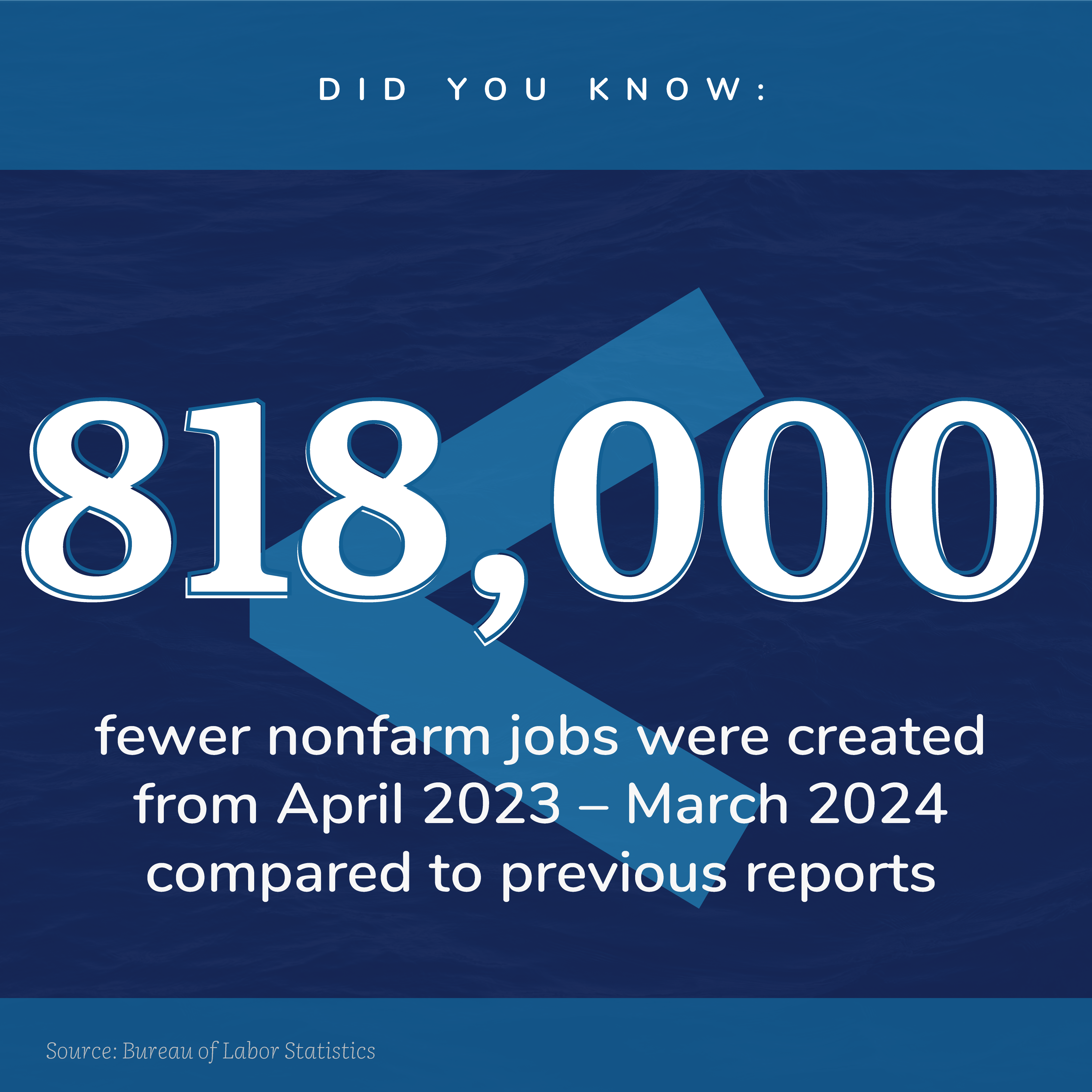

In Episode 60 of Talk Your Chart, Brett and Marcos dive into the economics of price gouging, the role of monopolies, and whether price caps could be the answer to rising costs. They also explore recent nonfarm job data, capex spending by the Magnificent 7, and recovering consumer sentiment. Join the conversation on what’s shaping…

-

Understanding Form 5500: A Guide for Business Owners

When it comes to managing your company’s retirement plan, one of the most important responsibilities is filing Form 5500. This form is crucial for maintaining compliance and protecting both your business and your employees. Let’s break down what Form 5500 is, why it matters, and share some practical advice on what to do if you’ve…