Why do experts call my 401k a “qualified plan”?

The quick answer is: A qualified plan is an employer-sponsored retirement plan that qualifies for special tax treatment under Section 401(a) of the Internal Revenue Code.

Now for some not too detailed details…

There are many different types of qualified plans, but they all fall into two categories. (1) Defined benefit plans (like a traditional pension plan) are generally funded solely by employer contributions and provide you with a specified level of retirement benefits. That specific level of benefit is why it is called a defined benefit plan. (2) Defined contribution plans (like a profit-sharing or 401(k) plan) are funded by employer and/or employee contributions. For these types of plans, only the contributions are defined as you don’t know exactly what the benefit will be in the future. The benefits you receive from the plan depend on investment performance and your and your employer’s contribution.

The annual contribution limits and other rules vary among specific types of defined benefit and defined contribution plans. However, most qualified plans share certain key features:

- Pretax contributions: Employer contributions to a qualified plan are generally able to be made on a pretax basis. That is, you don’t pay income tax on amounts contributed by your employer until you withdraw money from the plan. Your contributions to a 401(k) plan may also be made on a pretax basis.

- Roth contributions: Your employer may also allow you to make after-tax Roth contributions to the 401(k) plan. While there’s no up-front tax benefit, qualified distributions are totally free from federal income taxes.

- Tax-deferred growth: Investment earnings (dividends, interest, capital gains) on all contributions are tax-deferred. Again, you don’t pay income tax on those earnings until you withdraw money from the plan.

- Vesting: If the plan provides for employer contributions, those amounts (and associated investment earnings) must vest before you’re entitled to them. For example, a five-year graded vesting schedule could give 20 percent ownership after the first year, then 20 percent more each year until employees gain full ownership after five years. If the employee leaves before five years have passed, he or she only gets to keep the percentage that has been vested. One reason employers do this is to help retention.

- Creditor protection: A creditor is a person or company that you owe money to. In most cases, your creditors cannot reach your qualified retirement plan funds to satisfy your debts.

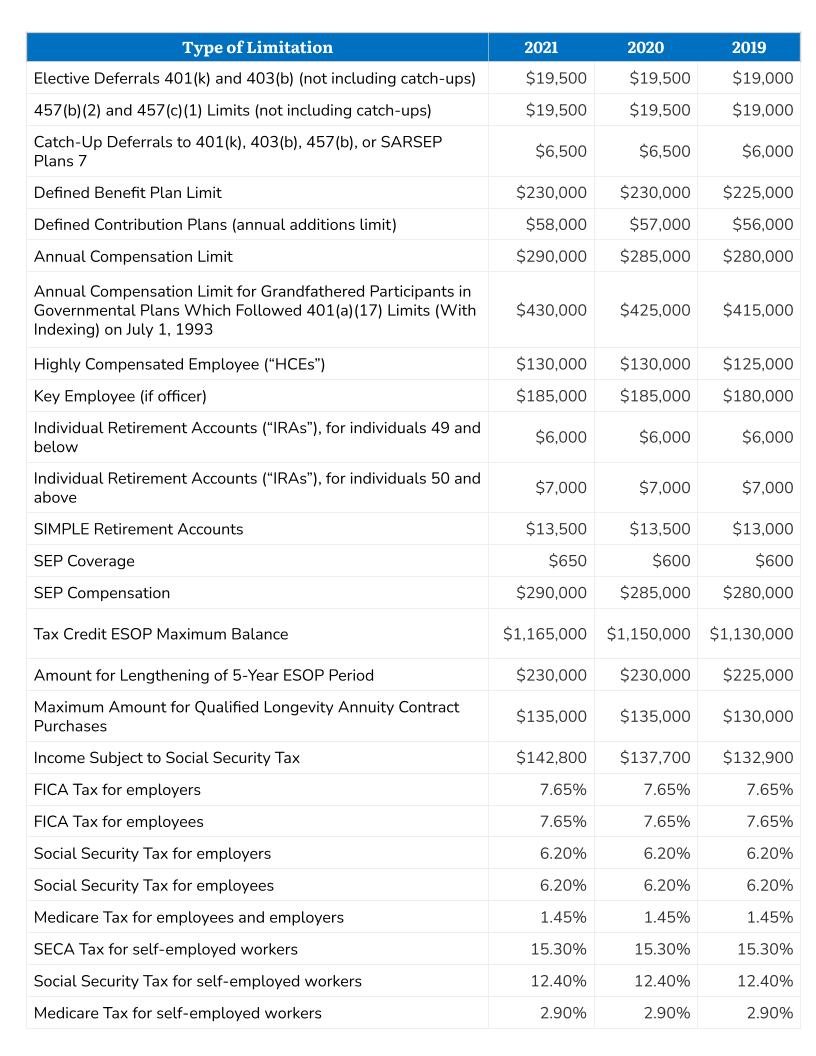

Lastly, I mentioned differences in annual contributions. Below is a breakdown of the different limits. Important to note that since traditional IRAs and Roth IRAs are not sponsored by an employer, they are technically not qualified plans. I’ve included past years for comparison purposes. Some of the “types of limits” may not be intuitive based on the name. That’s a good opportunity to reach out to us and find out what each means!

Happy Investing!

Marcos

Categories

Recent Insights

-

The Cost of a Good Idea — And What Golf Taught Me About Leaving It Alone

I started playing golf about a month ago. And let me be honest with you — it’s the most humbling thing I’ve done in recent memory. I grew up playing baseball, so I figured I’d have at least a fighting chance. The coordination, the swing mechanics — how different could it be? Turns out, very.…

-

Do You Own Your Time?

When a full calendar feels like success I am infamous for having a calendar booked for months in advance. When this first started happening, it felt good. Early in my career, I didn’t have enough work to fill my time, so the goal was simple: get as many meetings booked and clients closed as possible.…

-

Talk Your Chart | The Market Pullback, South Korea’s Rise, and the AI Trade | Ep. 79

In Episode 79 of Talk Your Chart, Marcos and Brett break down the market’s rare pullback, as they talk through the latest jobs report, interest rates, and what could pressure markets next. They also dig into the durability of the AI boom, South Korea’s rise as a global equity market, and how massive IPOs like…

-

The Financial Traits We Inherit (But Rarely Talk About)

A few years ago, I worked with a family going through a significant wealth transition. The parents had built a strong, disciplined financial life—steady investing, thoughtful planning, and a long-term focus. Their adult children? Very different. One avoided investing altogether and kept most assets in cash. The other leaned heavily into high-risk opportunities, always chasing…

-

Before the Bell Rings: The Most Important Back-to-School Conversations Aren’t About School

Every August, the same rituals play out in households across the country. Supply lists get checked off. Orientation nights get added to the calendar. New routines get tested. And couples spend a lot of energy making sure their kids are ready for the year ahead. What tends to get skipped? The conversation about whether they…