3 Market Considerations Heading into 2024

As we wrap up 2023, I want to discuss 3 points that are on my mind—and seemingly on the minds of folks like you: inflation, interest rates, and cash. As usual, the crystal ball is broken, but that won’t stop us from approaching things thoughtfully and with goals in mind.

1. Inflation: the next decade will probably look different than the last decade

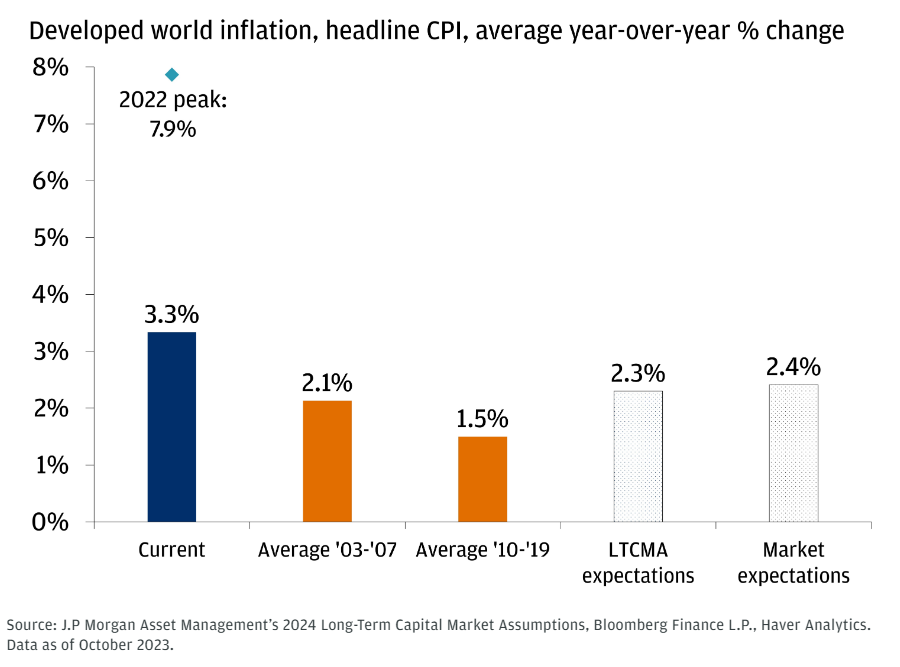

Reflecting on recent economic trends, we’ve observed a noteworthy shift in inflation across developed nations. Initially peaking at nearly 8%, headline inflation has now moderated to below 3.5%. This shift represents a significant change in the economic landscape. Various factors contribute to this outlook, including labor market dynamics. For instance, the labor market appears to be rebalancing, hinting at a possible moderation in wage growth. The rate of job creation is gradually slowing across multiple economies. In the U.S., the ratio of job openings to unemployed individuals has decreased, moving from nearly two-to-one a year ago down to approximately 1.3 to one today. This is only slightly higher than the pre-pandemic level of 1.2 to 1. Additionally, recent data on U.S. shelter costs—a significant component of the Consumer Price Index (CPI) —indicates an easing of housing inflation.

It’s essential to approach these observations with an understanding that they do not guarantee future outcomes. Factors such as industrial policies, the ongoing energy transition, and shifts in global supply chains (including the trend towards ‘nearshoring’) could influence commodity prices and limit reductions in the price of goods. Furthermore, consumer and investor expectations regarding inflation could play a role in shaping future inflationary trends.

As we navigate this evolving economic cycle, it’s reasonable to anticipate that the eventual ‘landing point’ for inflation might be higher than what we’ve experienced in recent decades. As with any economic environment, it is wise for investors to explore strategies that put you in a position to outpace inflation over time. The chart below compares the current rate of inflation across different time periods alongside market expectations and JP Morgan’s long-term capital market assumptions (LTCMA).

2. How much cash should be on my balance sheet?

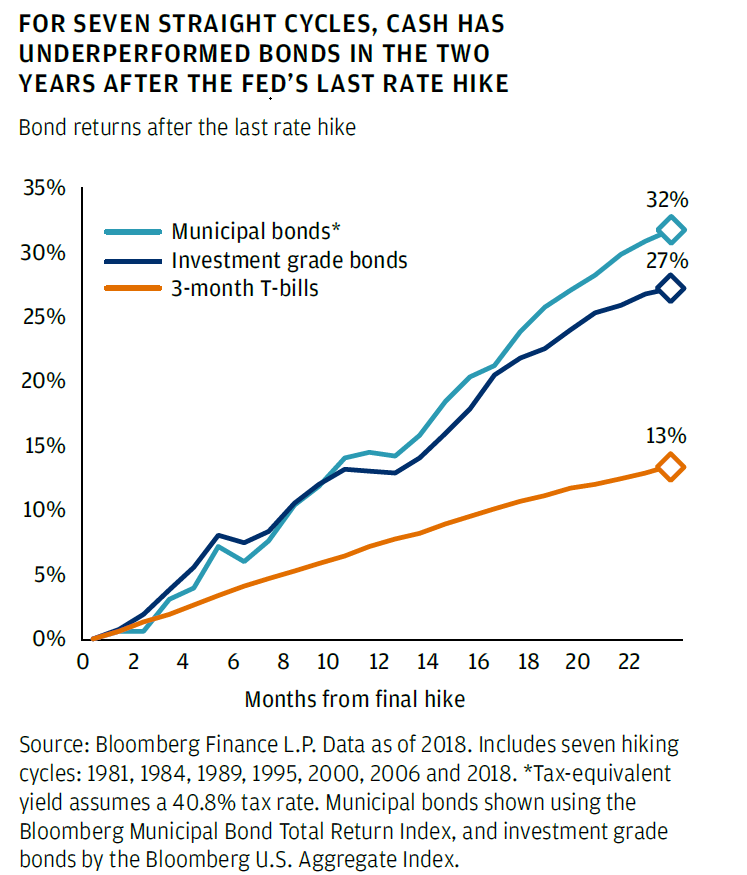

In the realm of financial planning, the role of cash (especially with a 5% yield) demands careful consideration. Historically, cash has shown its strengths in scenarios where central banks exceed expectations in rate hikes and when inflation anticipation is on the rise —a pattern that has developed over the past two years. However, the current economic climate presents a different picture. The conversation has notably shifted from speculating on further rate hikes by the Federal Reserve to a more focused anticipation of rate reductions in the upcoming year.

Let’s talk about rates and expectations. Currently, there’s a 60% probability assigned to a rate cut by March 2024, with a perceived certainty of a cut by May. By the end of 2024, the market anticipates a total reduction of 125 basis points. While these expectations may lean towards optimism, the underlying sentiment is clear: a general trend towards lower interest rates seems to be the consensus.

This shift has implications for cash holdings. With improving earnings growth forecasts and a rebound in risk sentiment, holding significant cash reserves could potentially lead to opportunity costs in the next phase of the economic cycle. Given the forward-looking nature of markets, one can argue that this is why we have seen a rally into year-end. Therefore, it’s crucial that investors reassess the role of cash within their broader, goal-aligned wealth management strategies. Understanding the role cash plays in your long-term objectives is key.

3. Bonds are back?

Recently, heightened bond performance has brought renewed attention to this asset class, especially in the context of U.S. core fixed income, which experienced its most favorable month in four decades this past November.

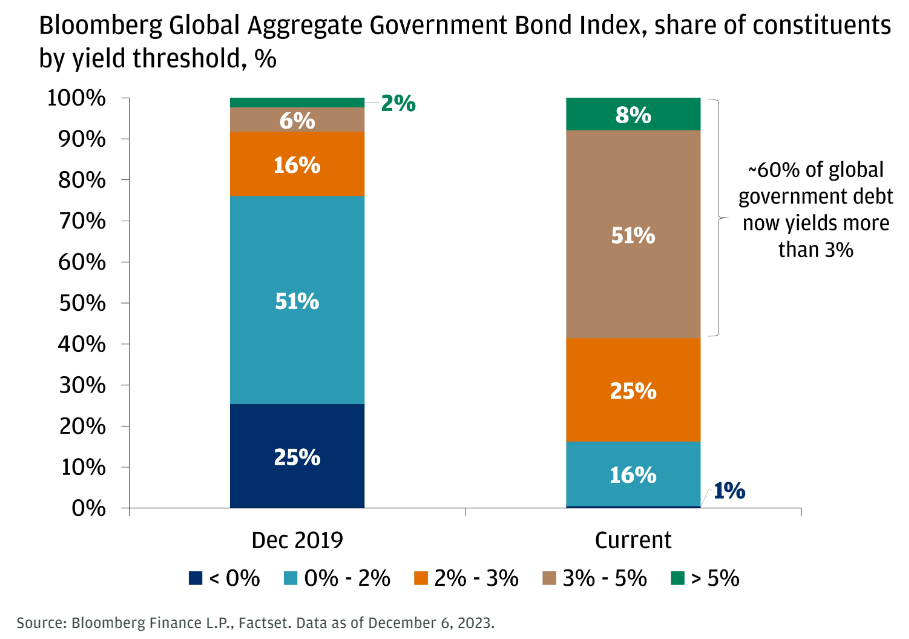

Bonds have traditionally been valued for their regular coupon payments that provide income for investors. The fundamental reason to own bonds in a broadly diversified portfolio has been two-fold: first, to smooth the ride (reduce fluctuation) and second, to fund the purchase of stocks when they’re down. In economic conditions characterized by slowing growth and declining interest rates, bond prices generally increase, adding to their appeal. However, this perceived security was not without its costs in the previous decade. Prior to the pandemic, a significant portion of global government debt (about 25%) was characterized by negative yields. This meant that investors were effectively paying to lend money —a situation more common in parts of Europe and Japan.

The landscape for bonds has undergone a significant shift recently. Negative yielding debt, once a widespread phenomenon, has drastically diminished and is now primarily confined to Japan. Interestingly, the Bank of Japan hinted this week at a potential departure from its negative interest rate policy in its upcoming meeting. This change is indicative of a broader trend in the global bond market. Currently, nearly 60% of global government debt offers yields over 3%, marking a stark contrast to the previous era of negative yields. This shift presents new opportunities and considerations for investors, who may now view bonds as a more attractive component in a diversified investment portfolio, especially in the context of higher yields and the potential for income generation.

I’ll end with two permanent truths: First, as usual, there is plenty to navigate going into a new year. Second, the key to arriving at your desired outcomes is to remain steadfast and focused on your long-term objectives. It’s important to align investment decisions with these goals. By maintaining a clear vision of your long-term ambitions, you can strategically position your portfolio to capitalize on the opportunities of 2024 and beyond. We live in a timing/selection culture; don’t fall victim. We will always encourage an approach that is goal-focused and planning-driven.

Happy investing!

Marcos

Sign up for our newsletter to receive more financial insights from our experts.

Categories

Recent Insights

-

Alternative Investments in 401(k) Plans: What Every Plan Sponsor Should Know

For decades, most retirement plans have followed a familiar playbook: stock funds, bond funds, target date funds, and a stable value or money market option to round things out. That playbook is starting to change, and if you sponsor a retirement plan, it’s worth understanding why alternative investments in 401(k) plans are suddenly part of…

-

What’s for Dinner? The Power of a Weekly Planning Reset for Your Family—and Your Finances

“What’s for dinner?” It’s the question that shows up every single day—usually right when life feels the busiest. Sometimes I wonder how we ever managed family life and work life before the days of online ordering and curbside pickup. Back then, dinner didn’t just mean cooking—it meant carving out time to walk the grocery store…

-

Building an Effective New Hire Onboarding Process for RIA Firms

Most RIA leaders know the feeling. You’ve worked through the hiring process, aligned internally on the role, and finally brought the right person on board. The offer is accepted, the paperwork is moving, and it feels like a win. But in practice, what happens next often determines whether that hire becomes a long-term contributor or an operational strain. In…

-

When to “Trust” your kids: Balancing independence and support

Deciding when and how to distribute funds from a trust to your children is one of the most nuanced responsibilities in estate planning. It sits at the intersection of financial stewardship, emotional judgment, and long-term family values. The goal is rarely just about transferring money. It is about shaping outcomes: independence, resilience, opportunity, and security.…

-

Retirees have questions for financial advisers. Here’s what they want to know.

Roughly a third want advice for what to do with the money in their former workplace plan, while nearly 3 in 10 want a withdrawal strategy that turns savings into retirement income. Others seek help with taxes, long-term care planning, debt reduction, or estate planning.