Maximizing Your Roth IRA: Tax-Savvy Strategies for Long-Term Growth

Roth IRAs offer a unique advantage: tax-free growth and withdrawals. This tax benefit makes Roth IRAs ideal for holding high-growth investments. But how do you strategically maximize the potential of your Roth IRA? Let’s explore.

What Makes Roth IRAs Ideal for Growth Investments?

Imagine growing your wealth without worrying about future tax bills—this is the power of a Roth IRA. The combination of tax-free growth and withdrawals provides an unparalleled opportunity to optimize your portfolio, especially when holding investments with higher growth potential. By focusing on these benefits, you can set yourself up for long-term financial success.

Strategic Investment Allocation Across Account Types

At Evensky & Katz/Foldes, we strategically allocate investments between tax-deferred and taxable accounts based on three key factors. This ensures our clients achieve the most tax-efficient outcomes while optimizing returns over time.

The Key Factors to Consider for Tax-Efficient Investing

1. Tax Cost Ratio: A Measure of Tax Efficiency

This metric shows how much a fund’s annualized return is reduced by the taxes investors pay on distributions. The higher the percentage, the less tax-efficient the investment is.

2. Potential Capital Gain Exposure: Predicting Future Taxes

This estimate measures the percentage of a fund’s assets that represent gains. It indicates how much the fund’s assets have appreciated and can signal potential future capital gain distributions.

3. Expected Returns: Leveraging Tax-Deferred Growth

This represents the anticipated return based on historical rates. Investments with higher expected returns may benefit more from the tax-deferred growth offered by accounts like Roth IRAs.

Generally, investments with higher tax cost ratios, higher potential capital gain exposure, and higher expected returns are best suited for tax-deferred accounts like Roth IRAs.

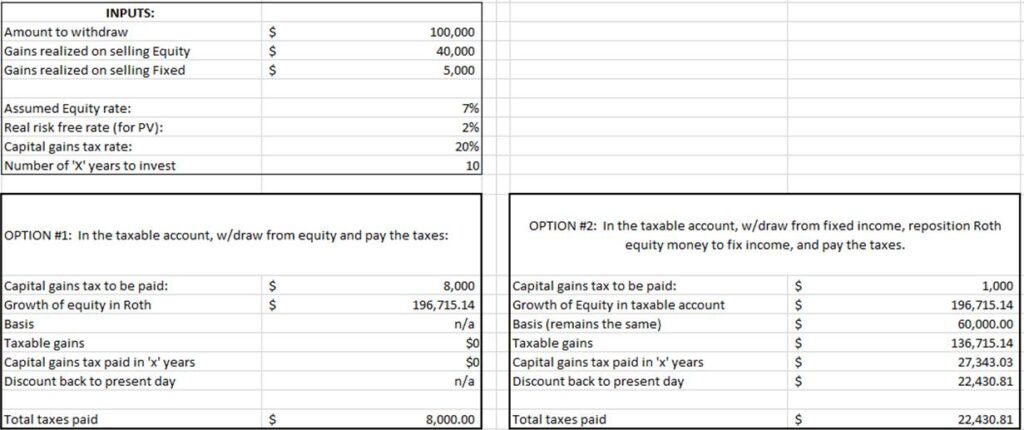

The Withdrawal Dilemma and why prioritizing is important:

Consider a scenario where you need to withdraw $100,000 from a portfolio with a 40% Fixed Income/60% Equity allocation. To maintain this balance, the withdrawal should come from the equity portion. You have two options:

Withdraw $100,000 from a taxable account, paying capital gains tax.

Reposition some Roth IRA funds from equity to fixed income, allowing for a $100,000 withdrawal from fixed investments, reducing capital gains tax.

In almost all cases, Option #1 is preferable. This approach minimizes the disruption to your tax-advantaged growth potential. Exceptions may arise if the investment time frame is very short or the equity growth rate is exceptionally low.

Why Long-Term Growth Belongs in Your Roth IRA

Keeping growth-oriented investments in your Roth IRA maximizes its tax-free growth potential. This strategy is particularly valuable for individuals with a long investment horizon, as the compounding effect can significantly amplify your portfolio’s value over time. By prioritizing growth assets in your Roth IRA, you create a tax-efficient foundation for future wealth.

At Evensky & Katz/Foldes, we understand that tax-efficient investing is a cornerstone of successful portfolio management. By carefully considering asset allocation and withdrawal strategies, we help our clients make the most of their Roth IRAs and other investment accounts.

Ready to take your retirement planning to the next level? Connect with us and start maximizing your financial future.

Categories

Recent Insights

-

Thoughtful Investing Through Diversification: Building Portfolios for an Uncertain World

Thoughtful investing requires more than selecting investments and letting them run. Portfolios evolve as markets move, risk shifts over time, and allocations naturally drift. Over time, even well-constructed portfolios can begin to behave differently than originally intended if they are not built and maintained with discipline. That discipline begins at the construction level. Diversification is…

-

Key Considerations Before Selling Real Estate in Florida: Taxes, Exemptions, and Planning Strategies

Selling real estate is often framed as a market decision—when to list, how to price, and whether conditions are favorable. Just as important, however, are the tax and planning implications that determine how much of the sale you ultimately keep. Whether you are selling a primary residence, a rental property, or a long-held investment, the…

-

Talk Your Chart | The Human Advantage | Ep. 78

In Episode 78 of Talk Your Chart, Marcos and Brett explore what today’s market is really responding to, from inflation and interest rates, to earnings, stock selection, and the growing role of AI. They discuss why successful investing often comes down to patience and behavior, and why human judgment, connection, and trust still matter in…

-

Are Property Taxes Going Away in Florida?

Florida property tax reform is a meaningful planning issue, but it is far from a done deal as there is currently no consensus plan from the Legislature to be put before voters in the upcoming November 2026 elections. Previous proposals have focused primarily on reducing — and in some versions ultimately eliminating — the non-school…

-

Is Wine an Investment? A Financial Advisor–Sommelier’s Perspective on Wine as an Alternative Asset Class

My professional life sits at the intersection of wealth management, wine, and winemaking—giving me a unique perspective on balancing long-term planning with the enjoyment of the journey along the way. As a wealth manager, sommelier, and winemaker, I’m often asked a deceptively simple question: Is wine a legitimate investment? My answer is always the same—it’s…