Why do experts call my 401k a “qualified plan”?

The quick answer is: A qualified plan is an employer-sponsored retirement plan that qualifies for special tax treatment under Section 401(a) of the Internal Revenue Code.

Now for some not too detailed details…

There are many different types of qualified plans, but they all fall into two categories. (1) Defined benefit plans (like a traditional pension plan) are generally funded solely by employer contributions and provide you with a specified level of retirement benefits. That specific level of benefit is why it is called a defined benefit plan. (2) Defined contribution plans (like a profit-sharing or 401(k) plan) are funded by employer and/or employee contributions. For these types of plans, only the contributions are defined as you don’t know exactly what the benefit will be in the future. The benefits you receive from the plan depend on investment performance and your and your employer’s contribution.

The annual contribution limits and other rules vary among specific types of defined benefit and defined contribution plans. However, most qualified plans share certain key features:

- Pretax contributions: Employer contributions to a qualified plan are generally able to be made on a pretax basis. That is, you don’t pay income tax on amounts contributed by your employer until you withdraw money from the plan. Your contributions to a 401(k) plan may also be made on a pretax basis.

- Roth contributions: Your employer may also allow you to make after-tax Roth contributions to the 401(k) plan. While there’s no up-front tax benefit, qualified distributions are totally free from federal income taxes.

- Tax-deferred growth: Investment earnings (dividends, interest, capital gains) on all contributions are tax-deferred. Again, you don’t pay income tax on those earnings until you withdraw money from the plan.

- Vesting: If the plan provides for employer contributions, those amounts (and associated investment earnings) must vest before you’re entitled to them. For example, a five-year graded vesting schedule could give 20 percent ownership after the first year, then 20 percent more each year until employees gain full ownership after five years. If the employee leaves before five years have passed, he or she only gets to keep the percentage that has been vested. One reason employers do this is to help retention.

- Creditor protection: A creditor is a person or company that you owe money to. In most cases, your creditors cannot reach your qualified retirement plan funds to satisfy your debts.

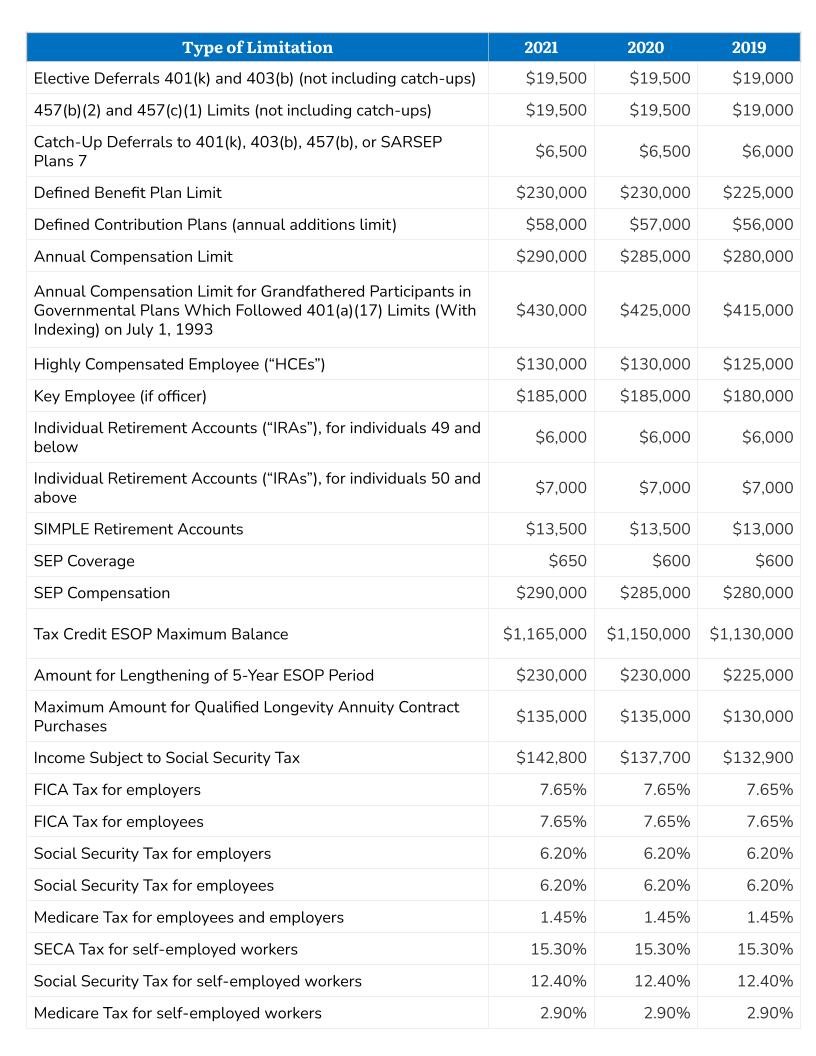

Lastly, I mentioned differences in annual contributions. Below is a breakdown of the different limits. Important to note that since traditional IRAs and Roth IRAs are not sponsored by an employer, they are technically not qualified plans. I’ve included past years for comparison purposes. Some of the “types of limits” may not be intuitive based on the name. That’s a good opportunity to reach out to us and find out what each means!

Happy Investing!

Marcos

Categories

Recent Insights

-

Smart Money Moves for Teens: The Best Financial Literacy Apps

Why Financial Literacy for Teens Matters Let’s face it—teaching teens about money can be tricky. But thanks to an ever-growing list of financial literacy apps, it’s never been easier (or more engaging) to help kids build healthy money habits. I recently spoke with two clients who’ve been using the Greenlight app to help their children…

-

Rebuilding Financial Confidence After Divorce: Managing Risk & Moving Forward

Divorce is not just an emotional transition—it’s a financial one, too. The process of separating assets, redefining financial goals, and adjusting to a new financial reality can feel overwhelming. But with the right mindset and strategies, you can regain control and build a future that aligns with your new chapter in life. Understanding Financial Risk…

-

Giving with Pride: Smart Strategies for LGBTQIA+ Donors

Understanding the Landscape of LGBTQIA+ Philanthropy LGBTQIA+ donors are uniquely positioned to drive meaningful change, but the philanthropic landscape remains complex and underfunded. Historically, LGBTQIA+ organizations have faced significant challenges in securing resources, often competing with larger, more established nonprofits for limited funding. This disparity highlights the importance of strategic giving to ensure that your…

-

How to Build Lasting Relationships that Propel Your Business and Elevate Your Community

As business leaders, our role in the community extends beyond charitable acts—it’s a strategic initiative that strengthens both our businesses and the communities we serve. Building meaningful community partnerships is not just about doing good; it’s about doing it strategically to foster deeper relationships, enhance your brand, and make a lasting difference. But where do…

-

Talk Your Chart | From Tax Trends to Firing a God Portfolio: Economic Insights | Episode 68

In Episode 68 of Talk Your Chart, Marcos and Brett dive into a jam-packed discussion of economic trends, market psychology, and long-term investing. From tax receipts and Social Security’s ticking clock to why even a ‘God’ portfolio gets fired—this one covers it all and more. Charts available for download here.